How Changing Mortgage Rates Affect Affordability

The Best Way To Keep Track of Mortgage Rate Trends

If you’re thinking about buying a home, chances are you’ve got mortgage rates on your mind. You’ve heard about how they impact how much you can afford in your monthly mortgage payment, and you want to make sure you’re factoring that in as you plan your move.

The problem is, with all the headlines in the news about rates lately, it can be a bit overwhelming to sort through. Here’s a quick rundown of what you really need to know.

The Latest on Mortgage Rates

Rates have been volatile – that means they’re bouncing around a bit. And, you may be wondering, why? The answer is complicated because rates are affected by so many factors.

Things like what’s happening in the broader economy and the job market, the current inflation rate, decisions made by the Federal Reserve, and a whole lot more have an impact. Lately, all of those factors have come into play, and it’s caused the volatility we’ve seen. As Odeta Kushi, Deputy Chief Economist at First American, explains:

“Ongoing inflation deceleration, a slowing economy and even geopolitical uncertainty can contribute to lower mortgage rates. On the other hand, data that signals upside risk to inflation may result in higher rates.”

Professionals Can Help Make Sense of it All

While you could drill down into each of those things to really understand how they impact mortgage rates, that would be a lot of work. And when you’re already busy planning a move, taking on that much reading and research may feel a little overwhelming. Instead of spending your time on that, lean on the pros.

They coach people through market conditions all the time. They’ll focus on giving you a quick summary of any broader trends up or down, what experts say lies ahead, and how all of that impacts you.

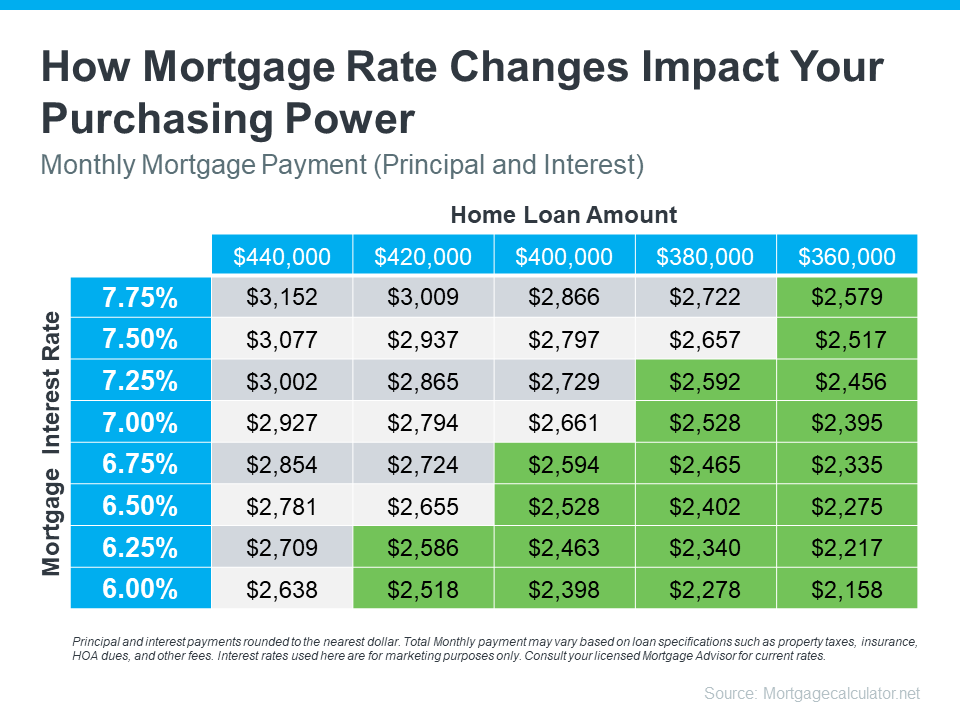

Take this chart as an example. It gives you an idea of how mortgage rates impact your monthly payment when you buy a home. Imagine being able to make a payment between $2,500 and $2,600 work for your budget (principal and interest only). The green part in the chart shows payments in that range or lower based on varying mortgage rates (see chart below):

As you can see, even a small shift in rates can impact the loan amount you can afford if you want to stay within that target budget.

It’s tools and visuals like these that take everything that’s happening and show what it actually means for you. And only a pro has the knowledge and expertise needed to guide you through them.

You don’t need to be an expert on real estate or mortgage rates, you just need to have someone who is, by your side.

Bottom Line

Have questions about what’s going on in the San Antonio area housing market? Let’s connect so we can take what’s happening right now and figure out what it really means for you.

San Antonio Home Sales Numbers Surged Again in February

Following an 11% increase in home sales in January, San Antonio home sales activity continued to strengthen in February

The number of single family homes sold in the San Antonio area in February was up 14%, compared to February 2023 with 2,697 homes sold, as reported by the San Antonio Board of REALTORS (SABOR) Multiple Listing Service Report.

Average and Median Home Prices – Despite the increase in the number of homes sold, the average price of homes sold in the San Antonio was 3% lower than February 2023. The average price of a home sold in the San Antonio area in February was $348,961. The median price homes sold for in February was $295,000, a 3% decrease compared to one year ago.

Average sold price per square foot in February was $173, which was 1%, lower than the average price per square foot in February 2023. Broken down between existing homes and new construction, existing homes sold for an average of $174 per square foot and new construction homes sold for an average of $170 per square foot in February.

Days on Market – Single family homes in the San Antonio area stayed on the market for an average of 80 days in February which was 11% eleven percent longer than in February 2023.

List Price to Sales Price Ratio – On average, homes sold for 93.1% of their original list price in February. This is up slightly from the average of 92.6% of their original list price that homes sold for in January.

Condominium and Townhomes – The number of Condominium and townhomes sold in February was 33% lower than one year ago with a total of 35 units sold. The average sold price of condos and townhomes, at $273,634 was 12% twelve percent higher than in February 2023.. Condominiums and townhomes stayed on the market for an average of 57 days in February, which was 8% eight percent less time than condos stayed on the market in February 2023.

Housing Inventory – At the end of February, there were approximately 4.3 months of inventory available for sale in the San Antonio area, so we are moving to a more balanced market. In February there were 4,011 new listings and of those, 2881 were resale homes and 1,130 were new construction. There were a total amount 11,974 homes on the market. The total number of new construction home listings at 4,120 was 6% higher than in February 2023.

New Home Sales Data – One of the most interesting trends over the past year is the increase in new home sales. The number of new construction homes sold in February was 39% higher year over year. The San Antonio new construction market has risen to meet the needs of homebuyers by increasing inventory, building more homes in the price ranges that buyers are looking for and by offering pricing and financing promotions that have helped home buyers to get into homes.

In the San Antonio area we are fortunate to have a wide range of new construction homes available and currently many home builders are offering promotional pricing, closing costs assistance and interest rate buy downs to help home buyers to get into a home. If you would like to learn more about new construction homes, you can easily search for available and to be built new construction homes and communities at https://www.showingnew.com/trudyedwards.

If you are home buyer, looking to get into a new home, but have concerns about interest rates and home affordability, here are a few things to consider. there are still lots of options available to help you get into a home such as low down payment mortgage programs, builder promotions, down payment assistance programs and creative financing strategies available to help home buyers get into a home with a more affordable monthly payment.

If you would like to learn more about down payment assistance programs and available options, contact your trusted mortgage lender or reach out to me for more information and recommendations for local lenders that can help match you to the best lending options for you.

Even if you are not quite ready to buy right now, if it’s your goal to buy a home this year, you can take steps to buying your first home and building generational wealth, by setting your goals, making a plan, taking steps to manage your finances, improving your credit and staying informed so that you’ll be ready to move forward when the opportunity arises.

If you want to make a move but have a home to sell before you can buy your next home, I have lots of options to help you sell your home with less stress and more money in your pocket!

A lot of homeowners today are sitting on tremendous home equity. But some homeowners have not been able to access that equity to make needed home repairs. Perhaps you have been putting off selling your home because you haven’t been able to make the repairs or cosmetic updates that would make your home desirable to the biggest pool of buyers. I can help you with that! Contact me today for a no obligation home seller consultation and we can review your options, including making home improvements with no upfront costs, payment at closing.

Whether you are thinking of buying a new construction home, buying your first home, or selling your your current home, it pays to work with a trusted real estate professional with local market insights. If you are ready to make your next move in the San Antonio area, reach out today for a no obligation home buyer or seller consultation with Trudy Edwards, REALTOR with Keller Williams Heritage.

Browse San Antonio area new construction homes and floorplans at ShowingNew.com/TrudyEdwards

** Percentage increases are based on a year-over-year comparison of February 2024 in comparison with February 2023. San Antonio market data provided by San Antonio Board of REALTORs

San Antonio Home Sales Numbers Surged Again in February

Following an 11% increase in home sales in January, San Antonio home sales activity continued to strengthen in February

The number of single family homes sold in the San Antonio area in February was up 14%, compared to February 2023 with 2,697 homes sold, as reported by the San Antonio Board of REALTORS (SABOR) Multiple Listing Service Report.

Average and Median Home Prices – Despite the increase in the number of homes sold, the average price of homes sold in the San Antonio was 3% lower than February 2023. The average price of a home sold in the San Antonio area in February was $348,961. The median price homes sold for in February was $295,000, a 3% decrease compared to one year ago.

Average sold price per square foot in February was $173, which was 1%, lower than the average price per square foot in February 2023. Broken down between existing homes and new construction, existing homes sold for an average of $174 per square foot and new construction homes sold for an average of $170 per square foot in February.

Days on Market – Single family homes in the San Antonio area stayed on the market for an average of 80 days in February which was 11% eleven percent longer than in February 2023.

List Price to Sales Price Ratio – On average, homes sold for 93.1% of their original list price in February. This is up slightly from the average of 92.6% of their original list price that homes sold for in January.

Condominium and Townhomes – The number of Condominium and townhomes sold in February was 33% lower than one year ago with a total of 35 units sold. The average sold price of condos and townhomes, at $273,634 was 12% twelve percent higher than in February 2023.. Condominiums and townhomes stayed on the market for an average of 57 days in February, which was 8% eight percent less time than condos stayed on the market in February 2023.

Housing Inventory – At the end of February, there were approximately 4.3 months of inventory available for sale in the San Antonio area, so we are moving to a more balanced market. In February there were 4,011 new listings and of those, 2881 were resale homes and 1,130 were new construction. There were a total amount 11,974 homes on the market. The total number of new construction home listings at 4,120 was 6% higher than in February 2023.

New Home Sales Data – One of the most interesting trends over the past year is the increase in new home sales. The number of new construction homes sold in February was 39% higher year over year. The San Antonio new construction market has risen to meet the needs of homebuyers by increasing inventory, building more homes in the price ranges that buyers are looking for and by offering pricing and financing promotions that have helped home buyers to get into homes.

In the San Antonio area we are fortunate to have a wide range of new construction homes available and currently many home builders are offering promotional pricing, closing costs assistance and interest rate buy downs to help home buyers to get into a home. If you would like to learn more about new construction homes, you can easily search for available and to be built new construction homes and communities at https://www.showingnew.com/trudyedwards.

If you are home buyer, looking to get into a new home, but have concerns about interest rates and home affordability, here are a few things to consider. there are still lots of options available to help you get into a home such as low down payment mortgage programs, builder promotions, down payment assistance programs and creative financing strategies available to help home buyers get into a home with a more affordable monthly payment.

If you would like to learn more about down payment assistance programs and available options, contact your trusted mortgage lender or reach out to me for more information and recommendations for local lenders that can help match you to the best lending options for you.

Even if you are not quite ready to buy right now, if it’s your goal to buy a home this year, you can take steps to buying your first home and building generational wealth, by setting your goals, making a plan, taking steps to manage your finances, improving your credit and staying informed so that you’ll be ready to move forward when the opportunity arises.

If you want to make a move but have a home to sell before you can buy your next home, I have lots of options to help you sell your home with less stress and more money in your pocket!

A lot of homeowners today are sitting on tremendous home equity. But some homeowners have not been able to access that equity to make needed home repairs. Perhaps you have been putting off selling your home because you haven’t been able to make the repairs or cosmetic updates that would make your home desirable to the biggest pool of buyers. I can help you with that! Contact me today for a no obligation home seller consultation and we can review your options, including making home improvements with no upfront costs, payment at closing.

Whether you are thinking of buying a new construction home, buying your first home, or selling your your current home, it pays to work with a trusted real estate professional with local market insights. If you are ready to make your next move in the San Antonio area, reach out today for a no obligation home buyer or seller consultation with Trudy Edwards, REALTOR with Keller Williams Heritage.

Browse San Antonio area new construction homes and floorplans at ShowingNew.com/TrudyEdwards

** Percentage increases are based on a year-over-year comparison of February 2024 in com

Your Credit Score Can be the Key to Your New Home

Understanding How Your Credit Score Impacts Your Mortgage Rate

Your credit score can affect your life in many ways, including whether you are approved for a home loan and your ability to get a good mortgage rate.

In this blog post, we’ll discuss what a credit score is, how it affects your mortgage rate, and how you can improve your credit score to get the best mortgage rate.

What is a Credit Score?

A credit score is a numerical figure that indicates how well you have managed your credit in the past. It is based on information from your credit report, which is a detailed report of your credit history. This includes the number and type of accounts you have, you bill payment history, including late payments, the age of the accounts and applications for credit that you have made. The most commonly used credit score is the FICO score, which ranges from 300-850 and is used by lenders to determine how risky it is to lend to you. Generally, the higher your credit score is, the more likely you are to be approved for a loan and to get a lower interest rate.

How Does a Credit Score Affect a Mortgage Rate?

Credit scores have a lot of impact on the interest rate you’ll be offered for a mortgage. When you apply for a mortgage, your credit score will be one of the main factors that lenders use to determine the interest rate they offer you. Generally, the higher your credit score is, the lower the interest rate you’ll be offered. This is because lenders view borrowers with higher credit scores as less risky, so they’re willing to offer them lower rates.

On the other hand, if your credit score is low, you may be offered a higher interest rate or even denied for the loan altogether. This is because lenders view borrowers with lower credit scores as more risky and are less likely to approve them for a loan.

How to Improve Your Credit Score

If you want to get a better mortgage rate, it’s important to take steps to improve your credit score.

Here is a list of the factors that make up your credit profile and some tips to help you improve your credit score:

- Payment History – Lenders are looking to see that you pay your bills on time. Late and missed payments can have a negative impact on your credit score, so make sure to pay all your bills on time. If you have automatic payments going out of your bank account it is best to make sure that your payments are set up to go out at least 3 days before the payment is due to make sure that the payment is credited to the account before it is due.

- Proportion owed versus Credit Limit – Don’t max out your credit cards. Having too much debt can also lower your credit score, so try to keep your credit utilization ratio (the amount of credit you’re using compared to the amount of credit you have available) as low as possible.

- Length of Credit History – The length of time that accounts have been open is part of your score. Don’t close unused accounts because that will not help your score. Apply for new accounts only as needed and don’t open too many new accounts in a short period of time. Lenders want to see a history of responsible credit management.

- Overall Credit Profile – Monitor your credit report. Be sure to check your credit report regularly to make sure there are no errors or fraudulent activities. If you find errors on your report you should inform the creditors and the credit bureaus and ask for your report to be updated. You can get a free copy of your credit report once a year from AnnualCreditReport.com.

How to Monitor Your Credit Score

In order to get the best mortgage rate, it’s important to monitor your credit score regularly. While you can request a free copy of your credit report from each credit bureau, once a year from AnnualCreditReport.com, but if you want to see your credit score, you can expect to pay an additional fee. However, check with your bank or credit card company first, as you free credit score monitoring is an added benefit that many companies are including these days.

You may also want to consider signing up for a credit monitoring service, which will alert you to any changes in your credit score. These services usually come with a small monthly fee, but they can be worth it if you want to stay on top of your credit score.

The Different Types of Credit Scores

There are actually several different types of credit scores, The most commonly used credit score is the FICO score, but there are also other types of credit scores, such as VantageScore and Experian.

It’s important to understand the different types of credit scores and how they are used by lenders. This will help you make sure you’re getting the best mortgage rate possible.

Understanding Your Credit Report

In addition to monitoring your credit score, it’s also important to understand your credit report. Your credit report contains detailed information about your credit history, including any late or missed payments, debts, and credit inquiries.

You can order all three reports at once or order them separately and space them out. It’s important to review your credit report regularly to make sure there are no errors or fraudulent activities showing up in your report. Your credit report will give you an overview of your credit history, so that you will be able to see if there are any areas that you need to improve or correct on your credit report, to help boost your credit score.

If you are planning to buy a home it can beneficial to talk to a trusted mortgage lender to review your credit report and score. They can often offer you advice on how to boost your credit score and will let you know how close you are, or whether you are ready to get pre-approved for a new home.

Conclusion

Understanding how your credit score impacts your mortgage rate is essential if you want to get the best rate possible. By taking steps to improve and maintain your credit score, you can be approved for credit and make sure you will be offered the best mortgage interest rate available. Keep in mind that it’s important to monitor your credit score regularly and understand how different types of credit scores are used by lenders. With a little effort and knowledge, you can get the best mortgage rate possible.

New Homes Continued to Boost San Antonio Market in December

Here is my latest San Antonio area real estate market update with the local real estate news you need to know, including the December 2023 year end real estate sales data and trends for the year ahead.

San Antonio homes sales were in December were down 3%, compared to December 2022 with 2,410 homes sold, as reported by the latest San Antonio Board of REALTORS (SABOR) Multiple Listing Service Report. However, breaking that down further, SABOR reported that while sales of resale homes were down by 10% year over year in December, sales of new construction homes were actually up by 29% when compared to December 2022.

Average and Median Home Prices – Despite the decrease in the number of homes sold in December, the average and median prices of homes sold in the San Antonio area were effectively unchanged year over year. The average price of a home sold in the San Antonio area in December was $373,797. The median price homes sold for in December was $319,113.

Average sold price per square foot in December was $177, which was unchanged from the average price per square foot in December 2022.

Days on Market – Single family homes in the San Antonio area stayed on the market for an average of 73 days in December, which was 20% twenty percent longer than in December 2022.

List Price to Sales Price Ratio – On average, homes sold for 92.7% ninety two point seven percent of their original list price in December.

Condominium and Townhomes – The number of Condominium and townhomes sold in December was unchanged from one year ago with 41 units sold. The average sold price of condos and townhomes, at $251,314 was 24% twenty four percent lower than in December 2022. Condominiums and townhomes stayed on the market for an average of 63 days in December, which was 40% longer than condos stayed on the market in December 2022.

Housing Inventory – At the end of December, there were approximately 4.3 months of inventory available for sale in the San Antonio area, so we are moving to a more balanced market. In December there were 2,771 new listings and of those, 1692 were resale homes and 1079 were new construction. The amount of new construction home listings was 55% higher than in December 2022.

New Construction Home Sales – One of the most interesting trends over the past year is the increase in new home sales. At the end of December 2023 the number of resale homes that sold in the San Antonio area for the whole year of 2023 was 23% lower than in 2022. However, at the end of 2023, the number of new construction homes sold was 39% higher year over year. The San Antonio new construction market has risen to meet the needs of homebuyers by increasing inventory, building more homes in the price ranges that buyers are looking for and by offering pricing and financing promotions that have helped home buyers to get into homes.

Interest Rates – In October 2023, the average rate for a 30-year fixed mortgage rate peaked at 7.79%. In January, that dipped to around 6.6% which was the lowest level since May of 2023. That downward trend in rates has made moving more affordable now than it was just a few months ago.

“Given this stabilization in rates, potential homebuyers with affordability concerns have jumped off the fence back into the market.”

Sam Khater, Chief Economist at Freddie Mac:

Experts are predicting that interest rates will continue gradually decreasing over the next few months. Dean Baker, Senior Economist, Center for Economic Research, recently remarked “It also appears that mortgage rates are now falling again. They will almost certainly not fall to pandemic lows, although we may soon see rates under 6.0 percent, which would be low by pre-Great Recession standards.”

If you are a home buyer contemplating a move but have concerns about high interest rates and home affordability, here are a few things to consider.

Experts are predicting that interest rates will continue gradually decreasing over the next few months. Dean Baker, Senior Economist, Center for Economic Research, recently remarked “It also appears that mortgage rates are now falling again. They will almost certainly not fall to pandemic lows, although we may soon see rates under 6.0 percent”

If you are home buyer, looking to get into a new home, there are still lots of options to help you reach that goal, including mortgage programs, builder promotions, down payment assistance programs and creative financing strategies available to help home buyers get into a home with a more affordable monthly payment. If you would like to learn more about down payment assistance programs and available options, contact your trusted mortgage lender or reach out to me for more information and recommendations for local lenders that can help match you to the best lending options for you.

One area of opportunity for home buyers right now is with new construction home as we are fortunate to have a wide range of new construction homes available rhroughout the San Antonio area and currently many home builders are offering promotional pricing, closing cost assistance and interest rate buy downs to help home buyers to get into a home. If you would like to learn more about new construction homes, you can easily search for available and to be built new construction homes and communities at https://www.showingnew.com/trudyedwards.

Even if you are not quite ready to buy right now, if it’s your goal to buy a home this year, you can take steps to buying your first home and building generational wealth, by setting your goals, making a plan, taking steps to manage your finances, improving your credit and staying informed so that you’ll be ready to move forward when the opportunity arises.

If it’s your goal to make a move in the San Antonio area and you’d like to talk more about the steps to help you reach that goal, reach out today for a no obligation home buyer or seller consultation with Trudy Edwards, REALTOR with Keller Williams Heritage.

3 Key Factors Affecting Home Affordability

Over the past year, a lot of people have been talking about housing affordability and how tight it’s gotten. But just recently, there’s been a little bit of relief on that front.

Over the past year, a lot of people have been talking about housing affordability and how tight it’s gotten. But just recently, there’s been a little bit of relief on that front. Mortgage rates have gone down since their most recent peak in October. But there’s more to being able to afford a home than just mortgage rates.

To really understand home affordability, you need to look at the combination of three important factors: mortgage rates, home prices, and wages. Let’s dive into the latest data on each one to see why affordability is improving.

1. Mortgage Rates

Mortgage rates have come down in recent months. And looking forward, most experts expect them to decline further over the course of the year. Jiayi Xu, an economist at Realtor.com, explains:

“While there could be some fluctuations in the path forward … the general expectation is that mortgage rates will continue to trend downward, as long as the economy continues to see progress on inflation.”

And even a small change in mortgage rates can have a big impact on your purchasing power, making it easier for you to afford the home you want by reducing your monthly mortgage payment.

2. Home Prices

The second important factor is home prices. After going up at a relatively normal pace last year, they’re expected to continue rising moderately in 2024. That’s because even with inventory projected to grow slightly this year, there still aren’t enough homes for sale for all the people who want to buy them. According to Lisa Sturtevant, Chief Economist at Bright MLS:

“More inventory will be generally offset by more buyers in the market. As a result, it is expected that, overall, the median home price in the U.S. will grow modestly . . .”

That’s great news for you because it means prices aren’t likely to skyrocket like they did during the pandemic. But it also means it’ll probably cost you more to wait. So, if you’re ready, willing, and able to buy, and you can find the right home, purchasing before more buyers enter the market and prices rise further might be in your best interest.

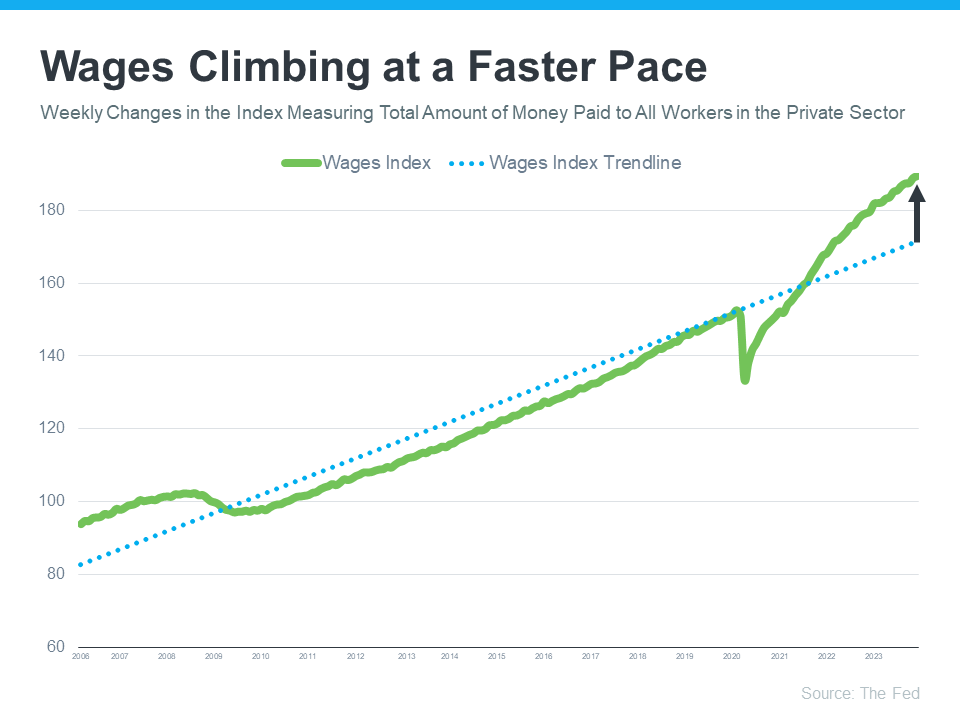

3. Wages

Another positive factor in affordability right now is rising income. The graph below uses data from the Federal Reserve to show how wages have grown over time:

If you look at the blue dotted trendline, you can see the rate at which wages typically rise. But on the right side of the graph, wages are above the trend line today, meaning they’re going up at a higher rate than normal.

Higher wages improve affordability because they reduce the percentage of your income it takes to pay your mortgage. That’s because you don’t have to put as much of your paycheck toward your monthly housing cost.

What This Means for You

Home affordability depends on three things: mortgage rates, home prices, and wages. The good news is, they’re moving in a positive direction for buyers overall.

Bottom Line

If you’re thinking about buying a home, it’s important to know the main factors impacting affordability are improving. To get the latest updates on each, let’s connect.

New Construction Homes in San Antonio Boosted Inventory and Sales in July

While July is often one of the busiest months for home sales, the number of single-family homes that sold in the San Antonio area in July was down 6% from the number of homes sold in July 2022 with 3,105 homes sold.

Average and Median Home Prices – However, the average price of a single family home sold in the San Antonio area in July, at $387,501 was the almost the same as the average price of a home that sold in July 2022 according to the Multiple Listing Service Report from the San Antonio Board of REALTORS. The median price homes sold for in July was $323,000 , which is a 2% decline compared to the July 2022 median price.

Average Price Per Square Foot – Average sold price per square foot in July was $182, which was 2% lower than one year ago. Breaking that down further single family existing homes, sold for an average of $182 per square foot, which was a 1% decrease compared to last year. Single family new construction homes also sold for an average of $182, which was 6% six percent lower than the average sold price per square foot that new construction homes sold for in July 2022. Single family homes in the San Antonio area stayed on the market for an average of 57 days in July which was 104% longer than in July 2022. On average, homes sold for 95.3% of their original list price in July, which was up slightly from the average of 95% of sales price in June.

Condominiums and Town Homes – The number of Condominium and townhomes sold in July was 1% higher than July 2022 with 81 units sold. The average sold price of condos and townhomes, at $254,294, was 4% higher than in July 2022. Condominiums and townhomes stayed on the market for an average of 61 days in July, which was 281% longer than the 15 days that condos stayed on the market in July 2022.

Housing Inventory – At the end of July there were approximately 3.8 months of inventory available for sale in the San Antonio area. The number of new listings was down by 17% seventeen percent in July, with only 4,258 new listings. There were 2,464 homes under contract at the end of June, which was down 18% from July 2022. At the end of July there were a total of 10,964 homes on the market in the San Antonio area, which was 25% higher than one year ago.

New Construction Homes – Over one third of the single family homes that went under contract in the San Antonio area in July were new construction homes, with 924 of the pending sales. San Antonio area builders have been taking action to help improve buyer affordability and increase sales by offering promotions such as special pricing and incentives such as promotional interest rates and rate buydowns. We are very fortunate in the San Antonio area, to have a large number of local and national home builders in our area, offering a wide range housing opportunities across a broad spectrum of areass and price ranges from multi-story town homes in the downtown area, afffordable two bedroom, no garage homes, to luxurious estate homes in master planned communities. New construction homes also have the added benefits of improved energy efficiency compared to many existing homes.

Whether you are thinking of buying a new construction home, buying your first home, or selling your your current home, it pays to work with a trusted real estate professional with local market insights. If you are ready to make your next move in the San Antonio area, reach out today for a no obligation home buyer or seller consultation with Trudy Edwards, REALTOR with Keller Williams Heritage.

Browse San Antonio area new construction homes and floorplans at ShowingNew.com/TrudyEdwards

** Percentage increases are based on a year-over-year comparison of July 2023 in comparison with July 2022. San Antonio market data provided by San Antonio Board of REALTORs.

More Jobs and Better Pay Leading to More Buyer Demand

There’s been talk about a recession for quite a while now. But the economy has been remarkably resilient. Why?

One reason is employment and wages have stayed strong. Let’s look at the latest information on each one and why both are good news if you’re thinking about selling your house.

More Jobs Are Being Created

Instead of facing the job losses typical of any recession, the economy has been growing and adding jobs. According to the Bureau of Labor Statistics (BLS), 187,000 jobs were created in July, which is up from the 185,000 created in June. That means more people are finding work. In fact, so many jobs are being added that the unemployment rate is far lower than the long-term average of 5.7% (see graph below):

A low unemployment rate means that most people who want to work are finding jobs. When people have jobs, they have steady incomes – and that can help set them up to consider homeownership.

People Are Making More Money

And data also shows hourly earnings have been going up pretty steadily over the past few years (see graph below):

When wages rise, people have more money that they could save or use toward buying a home. This increase in income helps offset some of the affordability challenges in the housing market today. Affordability depends on three main factors: wages, home prices, and mortgage rates. With higher home prices and mortgage rates right now, Builder Online summarizes how growing wages can help:

“The housing market has been a beneficiary of the strong economy and labor market. Many of those employed have saved money over the past few years and used those funds toward a down payment on a home.”

If you’re thinking about selling your house, a strong job market, growing wages, and the resulting buyer demand is fantastic news. It means there’s a larger pool of potential buyers out there who are in a position to pursue their dreams of homeownership.

Bottom Line

With more jobs and rising wages creating eager buyers, there’s a lot going in your favor. Let’s connect so you have someone who can guide you through the process of selling your house, from setting the right price to getting your home ready to show.

How Inflation Affects Mortgage Rates

When you read about the housing market in the news, you might see something about a recent decision made by the Federal Reserve (the Fed). But how does this decision affect you and your plans to buy a home? Here’s what you need to know.

The Fed is trying hard to reduce inflation. And even though there’s been 12 straight months where inflation has cooled (see graph below), the most recent data shows it’s still higher than the Fed’s target of 2%:

While you may have been hoping the Fed would stop their hikes since they’re making progress on their goal of bringing down inflation, they don’t want to stop too soon, and risk inflation climbing back up as a result. Because of this, the Fed decided to increase the Federal Funds Rate again last week. As Jerome Powell, Chairman of the Fed, says:

“We remain committed to bringing inflation back to our 2 percent goal and to keeping longer-term inflation expectations well anchored.”

Greg McBride, Senior VP, and Chief Financial Analyst at Bankrate, explains how high inflation and a strong economy play into the Fed’s recent decision:

“Inflation remains stubbornly high. The economy has been remarkably resilient, the labor market is still robust, but that may be contributing to the stubbornly high inflation. So, Fed has to pump the brakes a bit more.”

Even though a Federal Fund Rate hike by the Fed doesn’t directly dictate what happens with mortgage rates, it does have an impact. As a recent article from Fortune says:

“The federal funds rate is an interest rate that banks charge other banks when they lend one another money . . . When inflation is running high, the Fed will increase rates to increase the cost of borrowing and slow down the economy. When it’s too low, they’ll lower rates to stimulate the economy and get things moving again.”

How All of This Affects You

In the simplest sense, when inflation is high, mortgage rates are also high. But, if the Fed succeeds in bringing down inflation, it could ultimately lead to lower mortgage rates, making it more affordable for you to buy a home.

This graph helps illustrate that point by showing that when inflation decreases, mortgage rates typically go down, too (see graph below):

As the data above shows, inflation (shown in the blue trend line) is slowly coming down and, based on historical trends, mortgage rates (shown in the green trend line) are likely to follow. McBride says this about the future of mortgage rates:

“With the backdrop of easing inflation pressures, we should see more consistent declines in mortgage rates as the year progresses, particularly if the economy and labor market slow noticeably.”

Bottom Line

What happens to mortgage rates depends on inflation. If inflation cools down, mortgage rates should go down too. If you’re thinking of making a move in the San Antonio area, let’s talk so you can get expert advice on housing market changes and what they mean for you.

San Antonio New Construction Homes Boosted Inventory in May

New Construction homes in the San Antonio area gave a significant boost to local housing inventory

Read more about this and other San Antonio area real estate data and trends in this market update with the stats and trends for May 2023.

Average and Median Home Prices: Average home prices in the San Antonio area remained unchanged in May, compared to May of last year, according to the Multiple Listing Service Report from the San Antonio Board of REALTORS. The average price of a home sold in May in the San Antonio area, at $388,593, was the same as May 2022. The median price homes sold for in May was $324,750 dollars, which is a 3% three percent decline compared to May 2022 median price.

Sales Volume: The number of single-family homes that sold in the San Antonio area in May was down 3% percent from the number of homes sold in May 2022, with 3,487 homes sold.

Price Per Square Foot: Average sold price per square foot in May was $182 , which was 2% lower than one year ago. Breaking that down further single family existing homes, sold for an average of $183 per square foot, which was a 1% decrease compared to last year, while single family new construction homes sold for an average of $181, which was 7% seven percent lower than in May 2022 twenty twenty two.

Average Days on Market: Single family homes in the San Antonio area stayed on the market for an average of 65 days in May, which was 141% longer than in May 2022, but five days less than the average of 70 days that homes were staying on the market in April.

On average, homes sold for 95.2% of their original list price in May, which was up almost one percent from April.

Condominiums & Townhomes: The number of Condominium and townhomes sold in May was 33% lower than May 2022, with 78 units sold. The average sold price of condos and townhomes, at $281,973 was 1% one percent lower than in May 2022. Condominiums and townhomes stayed on the market for an average of 53 days in May, which was 2% two percent longer than condos stayed on the market in May 2022.

Housing Inventory: At the end of May, there were approximately 3.7 months of inventory available for sale in the San Antonio area, which is up very slightly from the 3.3 months of inventory that was available in April. The number of new listings was down by 1% in May, with 4,575 new listings. There were 2,887 homes under contract at the end of May, which was down 14% from May 2022. At the end of May there were a total of 10,005 homes on the market in the San Antonio area, which was 81% percent higher than one year ago.

New Construction Inventory: A significant amount of new listing inventory in May the San Antonio area came from new construction homes. There were 1,337 new construction homes added to the inventory in May which is up 52% from May 2022.

Market Overview: Even though we are still in a seller’s market, we are moving toward more of a balanced market, and today buyers have less competition and are gaining negotiating power.

Interest Rates and Mortgages: If you are a home buyer contemplating a move but wondering how and why to buy a home today, here are a few things to consider. While interest rates have increased from their historic lows, they are still far below where they have been in recent decades.

If you are looking to buy a home there are many mortgage programs, builder promotions, down payment assistance programs and creative financing strategies available to help home buyers get into a home with a more affordable monthly payment. If you would like to learn more about down payment assistance programs and available options, contact your trusted mortgage lender or reach out to me for more information and recommendations for local lenders that can help match you to the best lending options for you.

Whether you are thinking of buying a new construction home, buying your first home, or selling your your current home, it pays to work with a trusted real estate professional with local market insights. If you are ready to make your next move in the San Antonio area, reach out today for a no obligation home buyer or seller consultation with Trudy Edwards, REALTOR with Keller Williams Heritage.